Emmett Mulcahy, CPA, CVA

Emmett Mulcahy, CPA, CVA

Redpath Welcomes Eric Nelson as Advisory Services Partner

ST. PAUL, MN – July 1, 2026 – Redpath and Company is pleased to welcome Eric Nelson as a Partner and leader of the firm's Advisory Services practice.

Editor's note: this blog was updated in 2024 with additional resources for business owners.

Often, the business valuation process follows a similar story arc:

For business owners who take the valuation process seriously, a business valuation report is more than just a number. It’s a powerful document that provides deep insights into the company’s inner workings. If they engaged in a valuation process sooner, they could have influenced the “levers of value” and more successfully achieved their goals, e.g. maximizing their company’s value.Valuation Blog Series 1 of 3

Valuation Series 2: The Difference Between Business Calculation and Valuation Reports

Valuation Series 3: Business Valuation Approaches: Asset, Income and Market Approach

The process of obtaining a business valuation makes owners think critically about business operations , frame their understanding of the term “value” for more productive conversations, and most importanly, help them understand the relationship between the levers that drive value and how their business can adjust those levers.

At a high level, the levers that drive value can be broken down into company metrics, risk, and growth. Understanding these areas, and how they affect business valuation approaches, is key for business owners to maximize value.

Resource: Is Your Company an A Asset?

There are only three approaches to valuing a business: the asset approach, the income approach, and the market approach. For most businesses, the asset approach is not often used, as it is intended for businesses without a substantial intangible value. That leaves the income and market approaches.

These two ways to approach value are tied together in that, theoretically, the discount rate used in the income approach should be the inverse of the market multiple used in the market approach (adjusted for long-term growth).

Within the market approach, multiples are driven by two levers; risk and growth expectations. Given the relationship to the income approach, these two levers also drive the discount rate. By understanding the relationship between the income approach and market approach, we can see that any valuation conclusion comes down to the current company metrics, risk, and growth expectations.

Click here to read our ebook on Business Valuation →

In all business valuation services, the analyst starts by examining the current state of the company’s financial health.

While increasing revenues and improving profitability should typically lead to higher valuations, it’s helpful to review the factors that drive higher company metrics when looking to increase value.

Resource: The Transaction Abstract Podcast on What Can Increase or Decrease a Business’ Value

Resource: The Transaction Abstract Podcast on Raising Capital for Your Business

To understand the free cash flows of the company, valuation analysts start at the top of the income statement and work their way down. They then work through the cash flow statement. The insights garnered from each line item will cacade on the following line items and the conclusions generated by the analysts.

Analysts don’t just want to know that your company plans to grow, they want to understand how and what that growth looks like. For example, let’s say a company wants to grow 5% in the next year. Management should be able to discuss where that 5% will come from and what impact that has on the bottom line. This discussion should center on questions such as:

Developing a revenue growth strategy should help business owners fill in gaps for the rest of their financials. If new product services are part of the growth strategy, how will the new mix affect margins? Are current employee levels and facilities enough to absorb anticipated growth? What new selling and marketing expenses are required to help drive our revenue growth to hit our goal? Thinking along these lines will help business owners manage their net income and make changes necessary to help the bottom line increase.

Revenue growth typically requires investment in items like new equipment, new technology to help efficiency, buildings for more space, additional inventory, etc. To adequately fund growth, businesses need to reinvest in themselves and understand where that money is coming from. This is one of the most important metrics business owners need to understand.

While the profitability of a business should be the main driver for most of the reinvestment, understanding the collection and payable cycles helps gauge how much free cash flow the company actually generates.

Once you have an understanding of the metrics of the company, you next need to understand the risks associated with an investment in the company. There are two risk types that influence the expected return on investment; systematic and unsystematic risk.

To a large extent, the systemic risk cannot be adjusted by a business owner and is largely driven by the market. There is a spectrum of investment options where investors can invest their money, and each has an inherent risk profile in the market.

On one end of the spectrum are government-issued debts such as U.S. Treasury Notes, which are short-term debt obligations backed by the U.S. government. They are often considered risk-free, as the risk of default is deemed non-existent.

As you move across the spectrum of investments, additional risk factors are considered, increasing the rate of return. Other somewhat risky investments can include farmland, residential and commercial real estate, and corporate bonds.

When you get to equities as an investment class, financial risk—such as the quality and stability of earnings and the size of the entity—significantly influences overall risk. Larger companies typically carry less risk than smaller, non-publicly traded companies, for example.

Business owners should focus on the unsystematic risk associated with their company. This will include company-specific factors like:

While smaller, privately-held businesses always carry more risk than other investment options, addressing and limiting risk in the areas that business owners can control, can help maximize the value of their company.

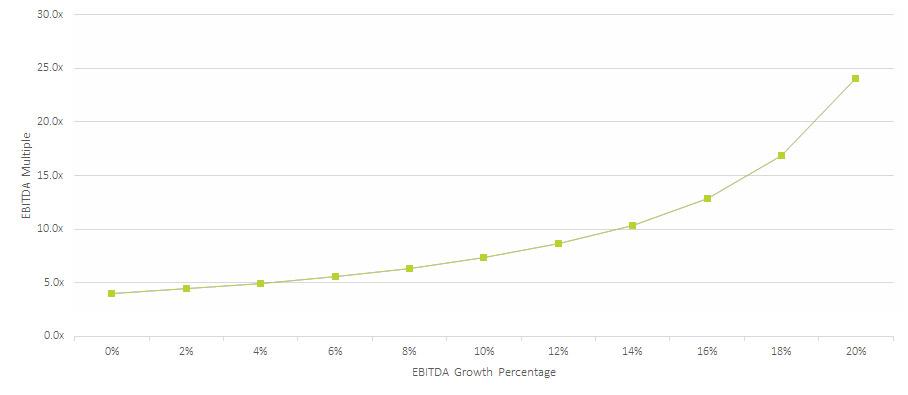

Growth plays an important role in a company’s value because all value is forward-looking. The more growth the company experiences, the more free cash flow the company can generate–which is attractive to a potential buyer.

Looking at growth from a purely mathematical basis, and holding all other considerations constant, growth will exponentially increase the multiples to be paid for by companies.

However, in practice, buyers will view growth differently, and their analysis will be shaped by the following factors:

Business owners, especially ones planning to sell their business, need to ensure that they have historical financial statements supporting their growth story, a documented growth strategy, and a plan to mitigate any potential risks along the way.

Understanding all the levers of value, and their effect on the business valuation, provides business owners with the knowledge and insights necessary to strategically drive more productive conversations, change operational strategy, and ultimately, realize more value for their business.

.jpg)

ST. PAUL, MN – July 1, 2026 – Redpath and Company is pleased to welcome Eric Nelson as a Partner and leader of the firm's Advisory Services practice.

Physician practice management is back in the conversation, but it is not the same market it was a few years ago. The surge in physician practice...

ST. PAUL, MN – June 23, 2026 – The M&A Advisor announced Jeremy Miller, a Managing Director in Redpath’s Transaction Advisory Services practice, as...